At two separate dinners in India, I put the same question to two men who have spent their lives inside this industry: where do the factories go when the sewing is automated?

The first is a large factory owner. His answer: production reshores to where the orders come from. Lead time, he told me, is so crucial, so essential to the brands, that once a factory can run without a labour cost penalty, it will stand next to its customer.

The second owns a buying office, the layer that sits between the brands and factories. His answer was the opposite, and he gave it without hedging: production stays in the textile clusters, for certain. A garment is not made by a garment factory alone. The fabric mill, the dye house, the trims and accessories, every input sits within reach of the sewing floor, and the infrastructure around those inputs means the garment factory itself must stay close to it.

Two men, one industry, opposite answers. I have spent eighteen months living inside this industry in Tiruppur, and before that six months visiting more than 45 garment businesses across eight countries, and I have never heard the question they were really arguing about stated out loud. It is not where the factories will go. It is what decides where factories go once the thing that has always decided it is gone.

For a century, the answer was labour. Not because labour is the biggest cost in a garment. It is not: standard garment costing puts fabric at 60 to 70 percent of a basic garment’s cost, with cutting, making and trimming a modest slice of the rest (INFLIBNET Centre, n.d.). Labour decides location because it is the cost that varies most by place. Fabric is traded, so its price converges across the world. Machines are traded too. Wages are not: a sewing operator in Tamil Nadu and a sewing operator in Bavaria have never cost the same. So the industry has spent a hundred years migrating along the wage gradient, from England to New England, to the American South, to Japan, to Korea, to China, to Bangladesh and to the city I live in. Automation does not remove the biggest cost. It removes the deciding one. That is why both men can be right about everything they see and still reach opposite conclusions, and it is why this essay exists.

What the machines can actually do

Before the argument, the honest state of the technology, because this essay is about a trajectory and not an arrival.

SoftWear Automation, the Atlanta company that has come closest to taking the human hand out of sewing, was founded in 2012 out of Georgia Tech with DARPA funding (Innovation in Textiles, 2026). In 2017 it announced a deal with Tianyuan Garments, then the largest sportswear producer for Adidas, to install 21 fully automated lines in Arkansas. The deal collapsed, and the company’s chief executive later described the commercialisation hurdles candidly in an interview with Wired (Innovation in Textiles, 2026). In August 2025 it closed a $20 million funding round led by BESTSELLER, the Danish group behind Jack & Jones and Vero Moda (BESTSELLER, 2025), and is intending to bring the third generation of its t-shirt line to market in 2026 (Sourcing Journal, 2025).

Fabric is limp. It folds, stretches, shears and slides in ways that metal and plastic do not, which is why sewing resisted the robot long after welding and painting were transformed. The machines are coming, and a major fashion group is now paying for them to come faster. But the fully automated garment factory has not arrived, and nobody has yet published the number that would settle whether it pays its way: an automated line’s capital, maintenance and Western overheads, counted honestly against Asian cut-make-trim. The unit economics are unproven, which is what makes BESTSELLER’s $20 million a bet rather than a rollout, and why this essay argues from direction rather than arrival. What has arrived is the question of where it will stand when it does.

Four times the machines moved

This question has been answered before. Four times, in four different ways, and the pattern across the four answers is the analytical core of everything that follows.

The first time, the machines were scarce, and production moved to the machines. In the early eighteenth century India was the world’s dominant textile exporter; the economic historians Clingingsmith and Williamson (2008) calculate that India produced about 25 percent of world industrial output in 1750 and about 2 percent by 1900. Their study attributes the collapse to a combination of forces: Britain’s enormous productivity gains in mechanised spinning and weaving, the transport revolution that collapsed freight costs, and India’s own domestic decline after the Mughal era. The detail that matters here is what did not save India: the world’s largest, cheapest, most skilled textile workforce. When machine productivity redefined the cost of cloth, the labour advantage that had clothed half the world counted for nothing. Production sat with the machines, the coal and the capital, because almost nobody else had them. This is the founding trauma of the industry I work in, and the first lesson: while the technology is scarce, location follows the technology and its energy source, and existing labour advantages are written off.

The second time, the machines commoditised, and production chased the remaining costs. By the 1880s anyone could buy textile machinery, and the American industry migrated from New England to the Carolinas and Georgia. The standard story is cheap Southern labour, and it is partly true, but Wright’s (1981) account in the Quarterly Journal of Economics is more useful than the standard story. Wright shows the Southern capture of the cotton textile market was driven by capital accumulation and by what he calls the maturation of the Southern labour force: a workforce that started cheap and unskilled, and compounded experience year over year while Southern mills installed newer machinery than the incumbents they were displacing. The market split along product quality, with the South taking coarse goods first and moving up. And Wright’s most surprising finding is how the story ended: the Great Textile Depression of the 1920s was caused not by demand or imports but by rising real wages in the South itself, the beginning of the chain that eventually sent the whole industry offshore. Second lesson: once the machines are equal everywhere, the largest remaining cost difference decides, the younger cluster out-invests the older one, and no wage advantage survives its own success.

The third time, labour left the cost stack entirely, and the industry moved to energy. Aluminium smelting is close to workerless, and electricity is its dominant input: the industry body European Aluminium puts energy at around 40 percent of primary production costs (Investment Monitor, 2022). The result is a geography that sounds absurd until you do the arithmetic. Bauxite is mined in Australia, shipped to smelters on Iceland’s eastern shore that run on hydropower priced roughly 30 percent below American rates, and the metal is then shipped onward to carmakers in the American Midwest (The New York Times, 2017). The United States, which once had more than thirty smelters, was down to five by 2017, and the reporting that documented the decline made a point worth keeping: the jobs mostly did not go to China (”Cheap Electricity Has Made Iceland,” 2017). They went to wherever the electrons were cheapest, including the Persian Gulf, where the regional aluminium council put energy at about a third of production expenses (Gulf News, 2012). Third lesson, and it answers a question I will return to: when labour is gone, shipping inputs across the entire planet is cheerfully accepted, provided one input dominates the cost stack and is dramatically cheaper somewhere else.

The fourth time, the binding constraint was knowledge, and automation concentrated the industry instead of dispersing it. A semiconductor fab is one of the most automated buildings humans have ever constructed, and on the aluminium logic fabs should scatter to cheap power. They did the opposite: they piled deeper into Taiwan, South Korea and Japan, into clusters of process engineers, equipment suppliers and accumulated tacit knowledge. The live demonstration is in Arizona, where TSMC repeatedly delayed its first American fab for want of enough workers with the specialised skills to install the equipment, a constraint its leadership acknowledged publicly more than once (Datacenter Dynamics, 2024). The fab eventually entered volume production in late 2024, behind its original schedule, and the site’s second plant is now targeted for 2027 (Focus Taiwan, 2026). Billions of dollars of subsidy, the most automated factory type on earth, and the pacing constraint was people. Fourth lesson: full automation does not free an industry from human beings. It changes which human beings the industry cannot do without, and those people might be scarcer than electricity.

Four moves, four destinations: the machines, the remaining costs, the energy, the knowledge. Which precedent applies depends entirely on the structure of what remains when labour drops out.

The new cost stack

Strip sewing labour out of a garment and what is left is this. The fibre and fabric, which were the biggest line all along. Energy. Machine capital and its depreciation. Maintenance and spare parts. Transport, which now means rolls of fabric inbound rather than finished garments outbound. Land, the cost of capital, regulation, and tariffs, the one line a government can rewrite overnight. And one line that looks small and is not: the handful of people who keep automated lines designing, running and recovering, who are the subject of this essay’s final argument.

Now audit who owns each line today, because the new ecosystem is not a blank map.

The input line points east. Polyester passed cotton in 2010 and now dominates: global fibre production reached 132 million tonnes in 2024, with polyester at 59 percent of it, around 78 million tonnes (Textile Exchange, 2025), and trade analyses put China at roughly 60 percent of global polyester output (Modaes Global, 2025). The fibre that clothes the world is, to a first approximation, a Chinese industrial product.

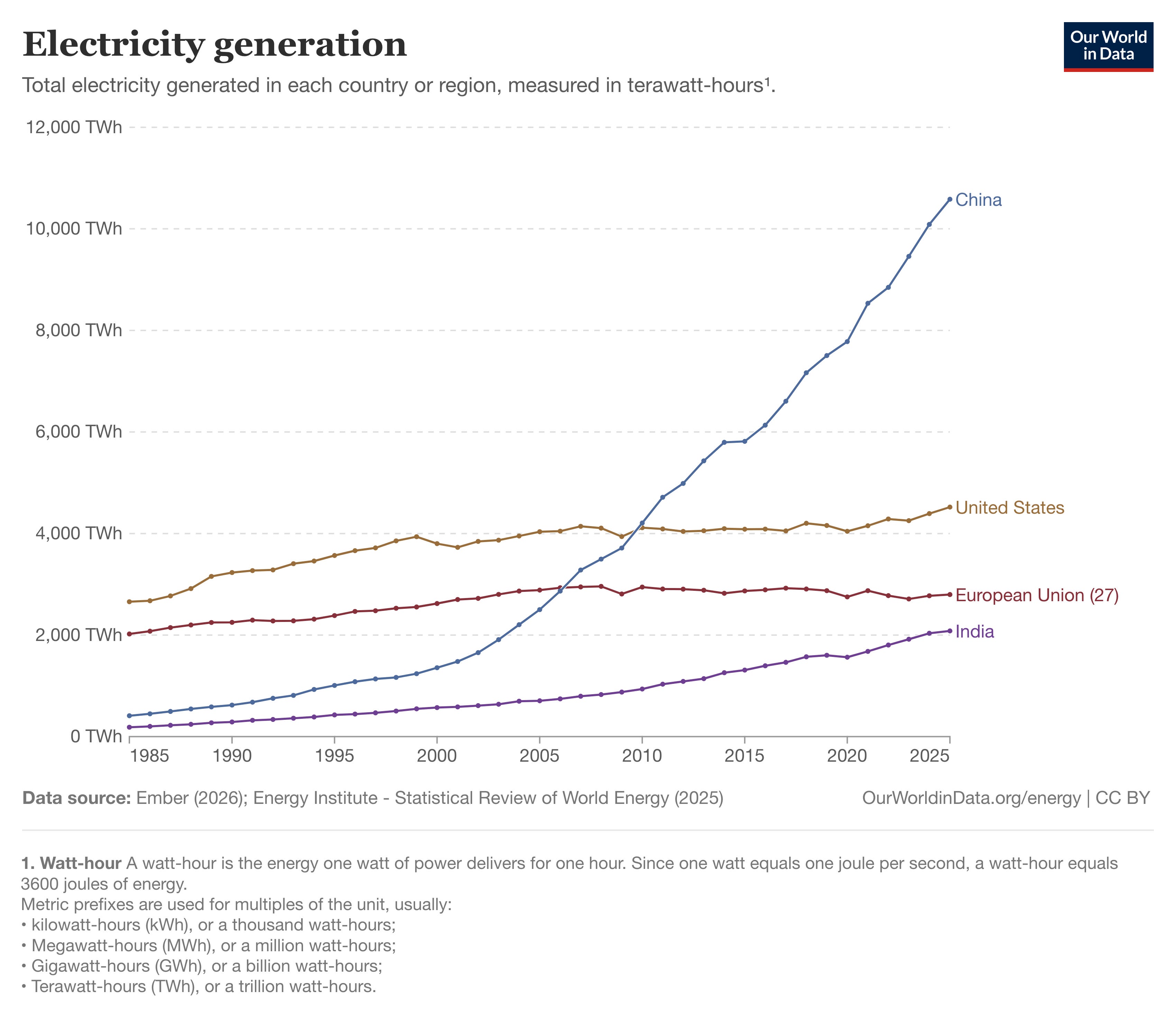

The energy line points the same way. China generated over 10,000 terawatt hours of electricity in 2024, more than the United States, the European Union and India combined, and over the past decade China added more new generation than Europe’s entire 2024 output (Energy Institute, 2025). Germany produces around 500 terawatt hours, a twentieth of China (Energy Institute, 2025).

Price matters as much as volume: electricity prices for energy-intensive industry in the European Union in 2023 ran at almost double the levels in the United States and China (International Energy Agency, 2024). For the sewing floor this is a rounding error. For the dye house it is the business model. Energy is also only half of the dye house’s siting problem. The other half is water and effluent regulation, and Tiruppur learned that the hard way: in 2011 the Madras High Court ordered more than 700 of the city’s dyeing and bleaching units closed over pollution of the Noyyal river, allowing them to reopen only on achieving zero liquid discharge (Down To Earth, 2011), and the industry rebuilt itself around recycling its own water (Scroll.in, 2016). Any country that wants the fabric stage must want its wastewater politics too.

The World Robotics 2025 report counts 542,000 industrial robots installed worldwide in 2024, with Asia taking 74 percent of them, Europe 16 and the Americas 9 (International Federation of Robotics, 2025a). China alone took 54 percent, its operational stock passed two million units, roughly 4.5 times Japan’s, after doubling in three years, and for the first time Chinese manufacturers sold more robots in China than foreign suppliers did (International Federation of Robotics, 2025b). Some talk about automation as the technology that ends China’s advantage. The installation data says China is buying the technology faster than everyone else combined.

And the stack has one line I have watched at close range: tariffs. I wrote earlier this year about what 50 percent tariffs do to factories running on 5 percent margins, and the lesson transfers directly. A tariff can outweigh every operational line on this list at the stroke of a pen, and unlike energy or fibre it is payable only at the border. In a post-labour cost stack, trade policy points the same way lead time does, toward the consumer market, because production inside the border pays none of it.

Cost against speed

Apply the aluminium test to garments. Aluminium ships bauxite from Australia to Iceland because one input is 40 percent of cost and is radically cheaper under a particular dam. Does any single line in the garment stack dominate like that? Fabric is the biggest line, but fabric is not dramatically cheaper in one place the way hydropower is; its cost advantage is diffuse, spread across China’s fibre, scale and energy position. Energy is decisive for the dye house but the dye house is a fraction of the garment. No single remaining input dominates the way electricity dominates a smelter. And when no cost line dominates, the other side of the scale gets its chance. The other side is speed.

Speed is worth more in clothing than in any metal, because demand for fashion moves weekly and demand for ingots does not. The careful version of this point needs a distinction the debate usually skips: there are two lead times. From-scratch lead time, from order to delivered goods, is dominated by the fabric stage and the ocean; sea freight alone commonly adds three to six weeks, and the fabric block is routinely the longest single stage (Wearview, 2026). Replenishment lead time, from seeing what sells to having more of it, is what brands actually compete on, and it is the one proximity transforms. The academic reference point is Ferdows, Lewis and Machuca (2004), whose Harvard Business Review study Rapid-Fire Fulfillment documented how Zara could design, produce and deliver a garment to the rack in fifteen days against an industry then working in months. Their explanation was not one technology but a holistic chain run on deliberately counterintuitive economics: factories held below capacity, small batches, trucks sent half empty, all to buy responsiveness. And the part of the Zara system that matters most for this essay is the fabric answer: Inditex applies postponement at the material stage, buying and holding undyed greige fabric, dyeing it only when demand declares itself, with roughly half its fabric suppliers belonging to the group itself (Aftab et al., 2018; Ferdows et al., 2004). Proximity sewing works because the fabric problem was solved first, with inventory, in-house dye and finishing capacity, and decades of textile knowledge in one region.

That is the standing proof of what speed is worth. Now the two attempts to buy it with robots instead of people. Adidas built exactly the factory the factory owner predicts: its Speedfactories in Ansbach and Atlanta, launched from 2016 with the automation firm Oechsler, were placed in consumer markets to collapse delivery times (adidas Group, 2016). Adidas makes shoes, not garments, but the location logic is identical, and in clothing the fabric problem is harder still, which makes the precedent conservative rather than loose. Adidas understood the fabric problem: at Ansbach a knitting machine produced the shoe’s upper material on site from yarn, lasers cut it, and soles were fused rather than glued (FashionUnited, 2016). Yarn in, shoe out, no mill in between. The staffing told its own story: around 160 employees against the 500 to over 1,000 typical of Asian footwear plants, hired against job profiles from industries like automotive rather than from footwear (Quartz, 2018). In November 2019 Adidas announced both plants would close by April 2020 and the technology would move to two suppliers in Asia, whose existing capabilities, the company said, would allow more product variations and better use of capacity (adidas Group, 2019). The retreat statement, as reported, named the destination’s advantages as the suppliers and the know-how (ThomasNet, 2020). Robots they could ship. The other two they could not.

The second attempt is the BESTSELLER bet on SoftWear, and it is narrower than Adidas’s was: automated sewing only, with no announced answer to the fabric question.

Meanwhile, the brands are not waiting for robots. They are buying speed today with the tool that already exists, nearby labour. The supply-chain auditor QIMA’s (2025) data shows nearshoring’s share of European sourcing portfolios at an all-time high in early 2025, with inspection demand in Morocco up 53 percent year on year and Egypt up 73; Inditex and H&M lean on Portugal, Morocco and Türkiye precisely for response time (CBI, 2026). The American side of the same data is the control group: Lu’s (2025) trade analysis at the University of Delaware finds no meaningful tariff-driven nearshoring to the Western hemisphere, with July 2025 apparel imports from Mexico up just half a percent despite the USMCA tariff advantage. Read the two columns together and the rule is clean. Brands buy speed wherever a capable labour pool sits near the consumer, and cannot buy it where one does not. Automation’s real promise is to break exactly that constraint.

The sharpest objection to this is Shein, which built the fastest fashion operation on earth from inside the Guangzhou cluster, with small-batch production digitally coordinated across its supplier network and air freight substituting for proximity. For a decade the model proved a cluster could out-deliver nearshoring. But part of its economics ran on a tariff loophole. The US de minimis exemption let parcels under $800 enter duty free, and a congressional committee estimated Shein and Temu alone accounted for more than 30 percent of those parcels (NBC News, 2025). Washington closed the exemption for Chinese goods in May 2025 and for the rest of the world that August (CNBC, 2025b; ExFreight, 2026), and low-value parcel volumes fell by more than half within four months (Marketplace, 2025). The fallout was measurable: Shein’s American sales fell 8 percent year on year in the first full month after the closure (Bloomberg, 2025), its full-year American sales declined for the first time since 2021 (Lu, 2026), and its response has been to build manufacturing in Turkey, Brazil and Mexico and expand American warehousing, which is to say to nearshore (CNBC, 2025a). Take away subsidised air freight and the cluster keeps its production tempo but loses its delivery advantage. Policy is pushing the fastest cluster model toward exactly the proximity logic this essay describes. Which returns us, one last time, to what the machines can and cannot carry.

The constraint that does not ship

Look back at the four precedents and notice what each destination had that could not be put on a ship. Britain had the machine builders themselves. The American South had the cotton and, in Wright’s (1981) account, a labour force compounding skill. Iceland has the dam. Taiwan has the machine builders again. Every migration in this story ran exactly as far as the unshippable thing allowed, and no further.

In garments the unshippable thing is know-how, and automation does not delete it. It splits it in two. The first half is the one I watch every day in Tiruppur: the craftsmen I sit with who take a fabric in their fingers and tell you the material and the GSM by touch, the people who know how garments in a factory behave as a system, what a particular knit will do under a particular needle. The second half is new: the robotics engineers, vision-system technicians and maintenance specialists who keep automated lines alive, the workforce TSMC could not find in Arizona. Here is the uncomfortable symmetry. The consumer markets have the second kind of know-how and almost none of the first. The clusters have the first kind and, on the IFR’s installation numbers, are acquiring the second faster than anyone, at least in China (International Federation of Robotics, 2025b). The place that already holds both was described precisely by the buyer who knows global manufacturing best. At the Fortune Global Forum in Guangzhou in December 2017, Tim Cook explained that Apple manufactures in China not for labour costs, which he said had stopped being low years earlier, but for the depth and concentration of skill, and above all for what he called “the intersection of craftsman kind of skill” with sophisticated robotics and computer science, an intersection he called very rare to find anywhere (Fortune, 2017; Leibowitz, 2017). Apple stayed for the intersection. Garment production will relocate exactly as fast as that intersection can be assembled somewhere else, and no faster. That is the cap, stated as plainly as I can state it: lead time and control are massive pull factors toward the consumer, and the pull is real, but it is rate-limited by people, not by capital, and assembling the people takes years in the best case. AI might help a lot with digitising and scaling tacit knowledge by training advanced vision systems and tactile sensors to essentially “feel” fabric tension and adjust machine parameters on the fly. If an algorithm can eventually codify how a lightweight jersey shears under a needle, rendering the master craftsman’s touch redundant, the geographical anchor of the textile cluster begins to erode. But translating the physical intuition of a human hand into a digital twin is the absolute frontier of machine learning, not its present reality. Until that software matures, the intersection of those two human skill sets remains the hardest constraint in the industry, and it will continue to dictate the map.

This matches what I have seen with my own eyes. In China, automation is everywhere, on the factory floors and in ordinary consumer life. In the factories I have walked through in Turkey, India and Bangladesh, production is still overwhelmingly manual. Advances are being made, but they are not comparable. The exceptions are standalone operations in a class of their own, Sri Lanka’s Brandix among them, and that class is found rarely outside China. The IFR’s numbers are not abstractions. You can see them from the shop floor.

Who wins

History says industries do not move as one block, so the honest answer comes segment by segment, from the stack and the speed premium.

Volume basics follow the aluminium logic toward inputs and energy, which means they mostly do not move at all. For basics like plain t-shirts, where fabric is 65 to 70 percent of cost (INFLIBNET Centre, n.d.), the winning location is wherever the fibre, the dye capacity and the cheap power already sit together, and automation deepens rather than ends China’s position there, because China’s advantage migrated off labour years ago. Cook said it in 2017; the robot installation data has been saying it every year since. What automation actually terminates is the advantage of places whose only card was the wage gradient.

Trend-responsive product follows the Zara logic toward the consumer, and this is where the factory owner is right and where the BESTSELLER bet lives. The working architecture already exists without robots: fabric held near the needle, dye and finishing capacity onshore, sewing close to the shop. Automation slots into that architecture as the replacement for the nearby labour pool it currently requires, which is precisely the constraint that has kept American nearshoring flat while European nearshoring booms.

And the exposed position belongs to the pure labour platforms, the locations whose entire pitch is the wage gap, with shallow fabric ecosystems and shallow machine skills. The precedents are unkind to that position in both directions: the South’s wage advantage died of its own success, and Bengal’s labour advantage died of someone else’s machines.

It depends on the good

So the answer to the dinner question is that there is no single answer. It depends on the good. Basics will concentrate where they can be made cheaply at scale, and on every line of the cost stack that place today is China. Trend product will, over the long term, sit close to the countries where it is sold. The Europeans already achieve this with capable labour nearby in Morocco and Türkiye. The Americans, who have no such labour pool, will get there through automation or not at all. Which leaves the constraint this essay keeps returning to: talent. Not the sewing, which the machines will take, but the craftsmen who know how to make a garment and a machine. Both men were right. They were just talking about different garments.

Every time the machines have equalised, the factories went to whatever the machines could not carry.

References

adidas Group. (2016). adidas expands production capabilities with SPEEDFACTORY in Germany [Press release]. https://www.adidas-group.com/en/media/press-releases/adidas-expands-production-capabilities-with-speedfactory-in-germany

adidas Group. (2019, November 11). adidas deploys Speedfactory technology at Asian suppliers by end of 2019 [Press release]. https://www.adidas-group.com/en/media/press-releases/adidas-deploys-speedfactory-technology-at-asian-suppliers-by-end-of-2019

Aftab, M. A., Yuanjian, Q., Kabir, N., & Barua, Z. (2018). Super responsive supply chain: The case of Spanish fast fashion retailer Inditex-Zara. International Journal of Business and Management, 13(5), 212. https://doi.org/10.5539/ijbm.v13n5p212

BESTSELLER. (2025, August 11). BESTSELLER invests in automated sewing robots [Press release]. https://bestseller.com/news/bestseller-invests-in-automated-sewing-robots

Bloomberg. (2025, October 10). Shein’s robust US growth evaporates after Trump tariff hit. https://www.bloomberg.com/news/articles/2025-10-10/shein-s-robust-us-growth-evaporates-after-trump-tariff-hit

CBI, Netherlands Ministry of Foreign Affairs. (2026, March 12). Which trends offer opportunities or pose threats in the European apparel market? https://www.cbi.eu/market-information/apparel/trends

Cheap electricity has made Iceland a leading aluminum producer. (2017, July 3). ArcticToday. https://www.arctictoday.com/cheap-electricity-has-made-iceland-a-leading-aluminum-producer/

Clingingsmith, D., & Williamson, J. G. (2008). Deindustrialization in 18th and 19th century India: Mughal decline, climate shocks and British industrial ascent. Explorations in Economic History, 45(3), 209-234. https://www.sciencedirect.com/science/article/abs/pii/S0014498307000447

CNBC. (2025a, May 6). Temu and Shein face massive tariffs. But don’t count them out of the U.S. e-tail scene, experts say. https://www.cnbc.com/2025/05/06/temu-shein-face-big-us-tariffs-dont-count-them-out-experts-say.html

CNBC. (2025b, July 30). Trump ends de minimis exemption for global low-cost goods. https://www.cnbc.com/2025/07/30/trump-de-minimis-shipping.html

Datacenter Dynamics. (2024, April). TSMC says Arizona fab is now ahead of schedule; signs semiconductor talent agreement with Kyushu University. https://www.datacenterdynamics.com/en/news/tsmc-updates-arizona-fab-production-timeline-signs-semiconductor-talent-agreement-with-kyushu-university/

Down To Earth. (2011). Tirupur dyeing units told to close. https://www.downtoearth.org.in/environment/tirupur-dyeing-units-told-to-close-33025

Energy Institute. (2025). Statistical review of world energy 2025. https://www.energyinst.org/statistical-review

ExFreight. (2026). De minimis rule 2025-2026: End of the $800 threshold for China imports. https://www.exfreight.com/de-minimis-rule-china-800-threshold-eliminated/

FashionUnited. (2016, May 25). Adidas: First Speedfactory to revolutionise production process. https://fashionunited.com/news/business/adidas-first-speedfactory-to-revolutionise-production-process/2016052511447

Ferdows, K., Lewis, M. A., & Machuca, J. A. D. (2004). Rapid-fire fulfillment. Harvard Business Review, 82(11), 104-110.

Focus Taiwan. (2026, January 15). TSMC’s Fab 2 in Arizona to begin mass production in 2nd half of 2027. https://focustaiwan.tw/business/202601150025

Fortune. (2017, December 5). Insights: Apple’s Tim Cook: China offers skilled – not cheap – workers [Video]. https://fortune.com/videos/watch/insights:-apple’s-tim-cook:-china-offers-skilled—not-cheap—workers/95a295a0-e456-4581-87a9-c7f1192a82ea

Gulf News. (2012). Aluminum firms seek cheaper production in Middle East. https://gulfnews.com/business/aluminum-firms-seek-cheaper-production-in-middle-east-1.1045760

INFLIBNET Centre. (n.d.). Apparel merchandising, Unit 6: Garment costing and pricing methods [Course material]. Vidya-mitra. https://vidyamitra.inflibnet.ac.in/data-server/eacharya-documents/56b0853a8ae36ca7bfe81449_INFIEP_79/52/ET/79-52-ET-V1-S1__unit_6.pdf

Innovation in Textiles. (2026, February 17). The return of the Sewbot! https://www.innovationintextiles.com/the-return-of-the-sewbot/

International Energy Agency. (2024). Electricity 2024: Executive summary. https://www.iea.org/reports/electricity-2024/executive-summary

International Federation of Robotics. (2025a, September 25). Global robot demand in factories doubles over 10 years [Press release]. https://ifr.org/ifr-press-releases/news/global-robot-demand-in-factories-doubles-over-10-years

International Federation of Robotics. (2025b, September 25). China: 2 million robots in factories [Press release]. https://ifr.org/downloads/press_docs/2025-09-25-IFR_press_release_China_in_English.pdf

Investment Monitor. (2022, October 31). Aluminium production is critical for the energy transition but hamstrung by high electricity costs. https://www.investmentmonitor.ai/sectors/energy/aluminium-production-energy-transition-challenges/

Leibowitz, G. (2017, December 21). Apple CEO Tim Cook: This is the No. 1 reason we make iPhones in China (it’s not what you think). Inc. https://www.inc.com/glenn-leibowitz/apple-ceo-tim-cook-this-is-number-1-reason-we-make-iphones-in-china-its-not-what-you-think.html

Lu, S. (2025). Statistics [Blog category]. FASH455 Global Apparel & Textile Trade and Sourcing, University of Delaware. https://shenglufashion.com/category/statistics/

Lu, S. (2026, February 4). Shein lost market share in the U.S. apparel retail market in 2025 amid trade tensions. FASH455 Global Apparel & Textile Trade and Sourcing, University of Delaware. https://shenglufashion.com/2026/02/04/shein-lost-market-shares-in-the-u-s-apparel-retail-market-in-2025-amid-trade-tensions/

Marketplace. (2025, December 26). How the end of the ‘de minimis’ exemption hit businesses. https://www.marketplace.org/story/2025/12/26/how-de-minimis-exemption-end-hit-businesses

Modaes Global. (2025, November 5). From China to India: The race to dominate global fiber production. https://www.modaes.com/global/markets/from-china-to-india-who-gives-more-fiber-to-the-world

NBC News. (2025, August 29). Retail panic: What the end of the ‘de minimis’ exemption means for brands across the globe. https://www.nbcnews.com/business/business-news/retail-panic-end-de-minimis-exemption-means-brands-globe-rcna227990

The New York Times. (2017, July 1). American companies still make aluminum. In Iceland.

QIMA. (2025). Nearshoring & reshoring trends: Recent data. https://blog.qima.com/traceability/nearshoring-reshoring-trends

Quartz. (2018, February 21). A German company built a “Speedfactory” to produce sneakers in the most efficient way. https://classic.qz.com/perfect-company-2/1145012/a-german-company-built-a-speedfactory-to-produce-sneakers-in-the-most-efficient-way/

Scroll.in. (2016, August 30). Can the courts save India’s rivers from pollution? Tirupur shows the answer is no. https://scroll.in/article/812470/can-the-courts-save-indias-rivers-from-pollution-tirupur-shows-the-answer-is-no

Sourcing Journal. (2025, August 15). SoftWear Automation secures $20M in Bestseller-led funding round to support scaling ‘Sewbots’. https://sourcingjournal.com/topics/financial/softwear-automation-bestseller-investment-series-b1-sewbot-commercialization-1234760204/

Textile Exchange. (2025). Materials market report 2025. https://textileexchange.org/knowledge-center/reports/materials-market-report-2025/

ThomasNet. (2020, November 5). Adidas faces colossal challenges to reshoring with 90% of its products manufactured in Asia. https://www.thomasnet.com/insights/adidas-reshoring/

Wearview. (2026). Lead time in apparel manufacturing explained [Glossary entry]. https://www.wearview.co/glossary/lead-time

Wright, G. (1981). Cheap labor and southern textiles, 1880-1930. The Quarterly Journal of Economics, 96(4), 605-629. https://doi.org/10.2307/1880743